- Home

- Media Kit

- MediaJet

- Current Issue

- Past Issues

- Ad Specs-Submission

- Reprints (PDF)

- Photo Specifications (PDF)

- Contact Us

- PRIVACY POLICY

- TERMS OF USE

Loading

![]()

ONLINE

Lewis Black

Tungsten Mining

Editors’ Note

Lewis Black is a Director, President, and Chief Executive Officer of Almonty Industries. Born in London, Black attended Manchester University and earned a BA degree in management and technology before joining a global insurance firm upon graduating. His career later shifted toward a focus on mining, and he has since accumulated more than 15 years of experience within the industry. Prior to Almonty’s founding in 2011, Black served as head of sales and marketing for SC Mining Tungsten, Thailand. He also held the roles of chairman and chief executive officer of Primary Metals Inc. (“PMI”), a former TSX-V listed tungsten mining company, between June 2005 and December 2007. As the founder of Almonty, Black has overseen the company’s rise to prominence as one of the foremost providers of tungsten within the global supply chain. Because of the dual high demand for tungsten and the difficulty associated with procuring it, Almonty and Black are highly sought-after for their expertise and access to the precious, widely used metal.

Company Brief

Almonty Industries (almonty.com) specializes in acquiring distressed and underperforming operations and assets in tungsten markets. These then benefit from the company’s in-house operational experience and expertise in the tungsten market. Highly regarded as a hands-on, turnaround investor-operator, Almonty is an expert at overseeing projects regarded as too complex or difficult for the average, pure “financial investor.” To date, the results of its acquisitions have been fast and very profitable turnarounds. Almonty is actively pursuing other growth opportunities via acquisitions where it can apply its tungsten expertise to create additional value for all stakeholders.

Workers at Almonty Industries’ tungsten mining operations

Will you highlight the history of Almonty Industries and how the company has evolved?

I founded Almonty Industries in 2011 after spending a few years working in the mining sector. I had the opportunity to focus on tungsten early on and became intimately familiar with its integral place in defense and consumer products as well as the rigid challenges that come with extracting it.

Our first acquisition was the Los Santos mine in the Salamanca province of Spain. Today, we also operate the Valtreixal deposit situated further north in Spain along with a site in Portugal. The Portuguese mine, Panasqueira, has actually been in more or less continuous operation for 126 years and is staffed by fifth-generation tungsten miners. While we’ve modernized much of the mining process and implemented stricter safety standards since it has come into our possession, we also rely on the knowledge that our staff brings which can only come from five generations of refining the mining process. That level of skill and familiarity is irreplaceable.

We are also in the process of reopening the Almonty Korea Tungsten Project (the Sangdong mine) in South Korea. This is a particularly exciting undertaking as it is one of the largest tungsten mines in the world and stands to substantially shift the politics involved with securing tungsten, as much of the global supply is sourced from China and Russia.

“Down the line, if our legacy as a company winds up being that we effectively preserved the last options for mining tungsten in transparent jurisdictions, then I think we’ll have done a great job.”

How do you define Almonty Industries’ mission and purpose?

We pride ourselves on standing alone in a highly niche but incredibly important field. Tungsten is pervasively used but hard to come by, although it’s a key component in critical, universally adopted products like cell phones, microchips, and automobiles, as well as defense, and it can only be sourced from an extremely limited range of locations.

Our primary aims are to address the rising global demand for tungsten by expanding the places it’s collected from and to elevate the methodology for mining to make it comparable to our competitors. Tungsten is a finite resource that happens to be extraordinarily difficult to process. Sourcing it requires assets, patience, and expertise, all of which Almonty happens to have in abundance. Unlike other mining companies, we specialize in a single commodity which has led to us succeeding where many others have failed when it comes to mining tungsten. We’re fortunate to have an institutionalized knowledge of this metal, and with it, a well-founded base upon which we can refine our process. Almonty has been able to compete with veteran suppliers from China because we’ve developed the best operational team in the world. Capacity-wise, we’ve been able to hone our mining operations to a point where we have the bandwidth to delicately navigate regulation considerations and potential areas for innovation and investments as well.

By opting for the specialist route over the jack-of-all-trades, master-of-none path, we’ve managed to get very good at doing a single thing really well. That’s the reason we’ve remained competitive and why we are well-situated to continue growing.

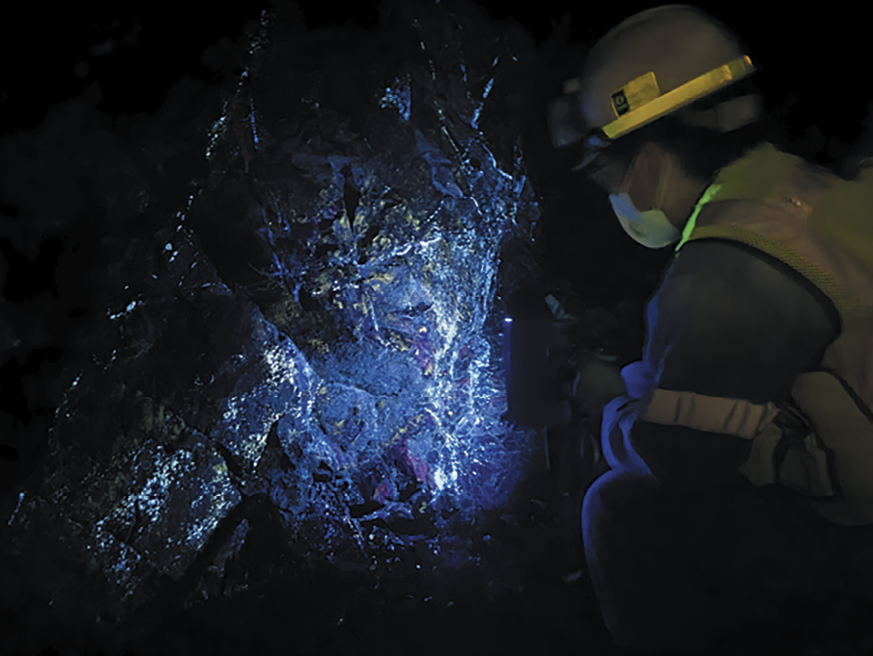

High-grade scheelite ore under UV light at the main

orebody in Almonty Industries’ Sangdong Tungsten mine

Where do you see the greatest opportunities for growth for Almonty and how will acquisitions fit into the equation?

Acquisitions don’t factor heavily into our plans for expansion – our forward momentum will come from internal growth as we develop the Sangdong mine in South Korea, which will in turn be fueled by the increasing geopolitical tensions we are all witnessing firsthand on a daily basis.

Almonty’s potential for growth is also dependent on the increasing government pressure surrounding strategic and critical metals along with the corresponding capital that is becoming available for them. Both the U.S. government and the European Union are now being extremely proactive in procuring alternate sources of supply, and as Almonty is the last man standing in tungsten mining, I anticipate that we will remain in extensive dialogues with both governments.

Will you discuss the critical role of tungsten in the defense sector?

Tungsten is a key material for manufacturing defense equipment. It’s widely used in manufacturing automotive parts and aerospace apparatuses – along with munitions – so it’s an essential resource for military purposes.

Roughly 12 percent of all tungsten is used in service of defense initiatives. Given the supply chain woes of the last few years, escalating geopolitical anxieties, and the relatively limited supply of tungsten, having control over how much of it is shipped and at what cost is a decisive position for any government, outwardly aggressive or otherwise, to be in.

Almonty tungsten drilling equipment

You mentioned that Almonty is on the verge of reopening the Almonty Korea Tungsten Project (the Sangdong mine), which hosts one of the world’s largest tungsten deposits and has the potential to produce a considerable percentage of the world’s supply. How do you describe the impact the Almonty Korea Tungsten Project could have on a macro level?

Operating at full capacity, the Sangdong mine could produce somewhere in the region of 15 percent of the world’s supply. It’s really the only viable, historically established source of tungsten that has emerged in the last decade. In terms of grade and size, few states have any long-term deposits with as proven of a track record as this particular mine has. Usually, the economic feasibility of resources is largely determined by reserves and quality. The average quality of the Chinese tungsten mine is 0.18 percent, while the quality of the Sangdong mine is 0.45 to 0.50 percent, which is the highest level and more than 2.5 times the global average. It is also competitive compared to other mines around the world in the production cost sector estimated based on the business feasibility model of Sangdong Mine. You would have to look to Russia or China for any comparable operations of this scale – with that in mind, the Sangdong mine is positioned to have a profound effect on diluting Western consumers’ dependency on outside sources for obtaining tungsten products and can allow U.S. manufacturers to avoid high tariffs on U.S.-imposed Chinese imports.

How is Almonty committed to sustainable mining practices?

It is our hope that regulatory bodies will recognize the need to balance the very pressing environmental concerns that ESG rules are meant to address alongside the geopolitical realities of 2023. As it pertains to mining, innovation that results in cleaner, safer practices is an unambiguously good thing. In order to stay ahead and remain competitive, mining companies should be exploring any and all avenues they have for incorporating more sustainable procedures.

With that said, the present clamor for tungsten in conjunction with long-standing regulations for both maintaining mines and establishing new ones can make it exceedingly challenging to enact immediate, meaningful changes. It’s our hope that as we engage in talks with entities like the U.S. and the EU that we’ll be able to devise practical sustainable practices that can be implemented effectively.

I feel strongly that an effective solution from a high-level perspective would be government-provided offtakes, loans, and subsidies. Incentivizing producers with additional access to state capital that could actually be put toward sustainable initiatives – rather than asking them to materialize the necessary funds out of the ether – could potentially address the myriad concerns of all involved parties.

What are your views on the importance of secure supply chains for critical minerals?

As we’ve all seen and personally felt, the last few years have raised serious questions about the effectiveness of the global supply chain as it’s currently constructed. In addition to the shipping issues brought about by COVID, the war in Ukraine and ensuing measures taken against Russia have critically undermined the traditional wisdom around sanctions. Despite attempts to shut Russia out of the market, the country’s exports – tungsten being among them – have still managed to enter circulation. Rather than going through the EU as it once would have, now it’s processed through China. It’s not a global supply chain: it’s a competing jurisdictions supply chain.

Given all of these well-documented problems and growing tensions among adversarial players, the need to reconfigure and bolster the supply chain’s security has never been stronger. If governments intend on being serious about protecting their defensive and economic assets, a major diversification in structure is sorely needed.

The EV battery manufacturing market is as fierce as ever with demand rapidly growing. Through all of this, it is worth noting that there are three major companies from South Korea, LG Energy Solution, Samsung SDI, and SK Innovation, making South Korea the second largest EV battery manufacturer. Unfortunately, manufacturers in South Korea have high reliance on Chinese tungsten in terms of supply chain. The tungsten reservoir that is the Sangdong Tungsten Mine will provide a shelter from the tightening supply influenced by various factors such as the pandemic, inflation, and Russia-Ukraine war. The Sangdong Tungsten Mine is ready to offer an opportunity to supply institutions and related industries with high-grade tungsten, at an affordable price, with a stable supply chain and well-established logistics systems.

Will you provide an overview of the geopolitical risks and defense implications of the tungsten industry?

Well, the supply chain concerns are directly intertwined with the geopolitical and defense considerations. Tungsten is mainly sourced from Russia and China and in the event either one of them chose to restrict their tungsten exports – whether by cutting off supplies or manipulating pricing – the rest of the world would have little in the way of alternatives for acquiring tungsten.

This tension is exacerbated by the present conflict between Russia and Ukraine. Tungsten is a crucial material for munitions production, and the West has largely lost the manufacturing infrastructure it once had. Now, entities have not only found themselves purchasing tungsten from adversarial forces, but are doing so with the intention of weaponizing it against the very people they bought it from in the first place.

Beyond the overt strangeness of this dynamic, the current situation is an effective, if unfortunate, illustration of tungsten’s importance and the risks of relying on competing powers for essential materials.

What do you see as the keys to effective leadership and how would you characterize your management style?

I think effective leadership is measured first and foremost by examining whether or not the person in charge can execute the plans that are laid down within the company. It’s only right that a manager’s effectiveness should be assessed based on their ability to deliver on their own projections.

As for my own management style, I would say that I lean more toward a blue-collar approach rather than a white-collar one in terms of how I operate. That’s mainly a reflection of the people I work with. I’m largely dealing with a group of predominantly male, tough-as-nails, hard-drinking, chain-smoking guys who don’t suffer fools gladly.

Almonty’s miners risk their lives navigating a hazard-heavy occupation and, even though we operate at extremely high safety levels, it’s still a very dangerous job to go underground and work the mines. It’s not risky like it used to be, but you have to have a certain personality to be able to tolerate the conditions of the job. Picture it: you’re in a pitch-black environment where it’s so dark that if you try to put your hand in front of your face, the only way you’ll know for certain it’s there is by feeling the warmth of your palm against your nose; you can’t see it. Plus, there’s no shortage of dust and it smells of diesel because of ventilation. So, for many, it’s a very alien, claustrophobic environment.

Needless to say, I work with tough guys, and they demand respect. If they don’t like their manager, they won’t work for them because they’ll feel their lives are at risk. It is vital that there is a shared, sincere respect between all parties. If I go in and give them a speech about something totally removed from their lives and on-the-job experience, they’re going to look at me like I’m out of my mind. I need to project that I’m cognizant of the procedures for operating their equipment as well as the geology and metallurgy concerning tungsten; they can’t trip me up.

In order to navigate all of that, you have to earn the respect of the team and of your colleagues who essentially risk their lives on a daily basis. It’s a very different dynamic from how corporate management traditionally operates. For all intents and purposes, the people I work with don’t check my manicure – they check my fists; they want to know that my hands have calluses, not manicured nails. Ultimately, you’ve got to be someone who’s not afraid to get their hands dirty. It’s one of the last careers or businesses where that’s really required.

What are your priorities for Almonty as you look to the future?

Down the line, if our legacy as a company winds up being that we effectively preserved the last options for mining tungsten in transparent jurisdictions, then I think we’ll have done a great job. We’ve already revitalized the knowledge around the practice of extracting and processing tungsten that seemed to have all but died out in the '80s and early '90s, so that’s been a commendable effort. Once mining at the Sangdong site is properly underway, we’ll have the ability to both preserve that knowledge and actively apply it in a working environment. Naturally, our mines in Spain and Portugal will continue operating as they have for some time now, but there’s enough raw material housed within the South Korean project for it to go on for more than 100 years. I think it’s significant for that knowledge to continue for another three generations – in my estimation, that’s something worth celebrating, because once it’s gone, it’s gone. There’s no specialized school you can go to; nobody runs courses on excavating tungsten, and the books that exist are spurious at best. I think Almonty’s future lies in our continued ability to deliver on the essential and singular service we provide, namely, preserving the knowledge around processing an immeasurably valuable and extremely difficult to extract metal.![]()