- Home

- Media Kit

- Current Issue

- Past Issues

- Ad Specs-Submission

- Ad Print Settings

- Reprints (PDF)

- Photo Specifications (PDF)

- Contact Us

Loading

![]()

ONLINE

Duncan L. Niederauer

A Global Platform

Editors’ Note

Duncan Niederauer was the Head of U.S. cash equities for NYSE Euronext before assuming his current post with the company. He joined the exchange in April 2007, and before this, was Managing Director and Co-Head of the Equities Division Execution Services for Goldman Sachs. Niederauer earned his B.A. from Colgate University and his M.B.A. from Emory University.

Company Brief

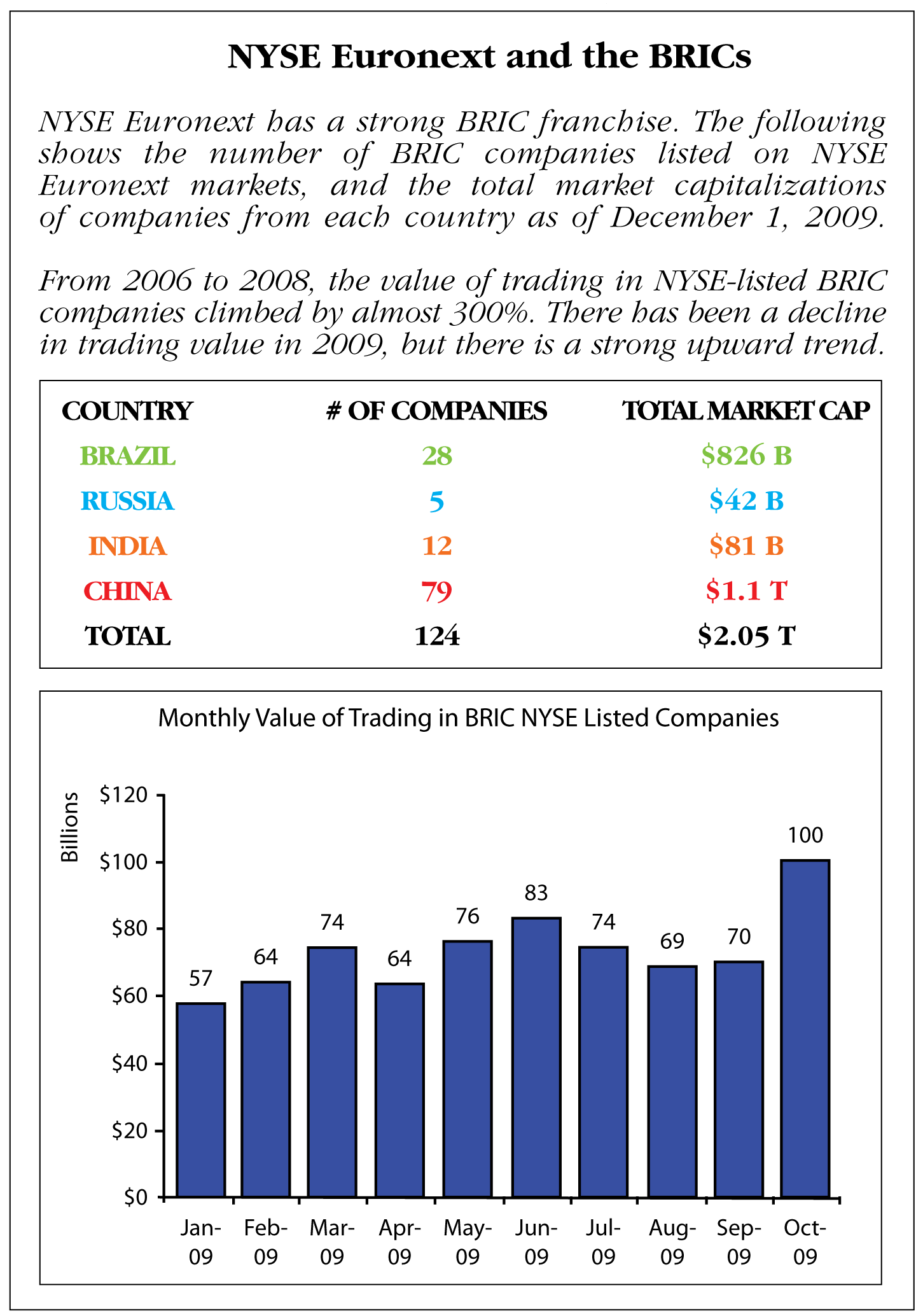

NYSE Euronext (www.nyx.com) is a leading global operator of financial markets and a provider of innovative trading technologies. The company’s exchanges in Europe and the United States trade equities, futures, options, fixed-income, and exchange-traded products. NYSE Euronext’s equities markets in Europe and the United States represent nearly 40 percent of the world’s equities trading and have more than 8,000 listed issues. NYSE Euronext’s equities market is the global leader in listings from BRIC countries by both number of companies – more than 120 – and total global market capitalization – $1.78 trillion. NYSE Euronext also operates NYSE Liffe, the leading European derivatives business and the world’s second-largest derivatives business by value of trading. The company offers comprehensive commercial technology, connectivity, and market data products and services through NYSE Technologies. NYSE Euronext is in the S&P 500 index, and is the only exchange operator in the S&P 100 index and Fortune 500.

Now that we are a little over a year into the economic crisis, are you comfortable that the situation has now stabilized?

The worst is certainly behind us, and recovery in the equities markets has people thinking that real economic recovery can’t be far behind. But if you travel around the world, it’s hard to find meaningful economic recovery outside of Brazil, India, and China. Other countries are talking about GDP growth in the second or third quarter of 2010, which is great, but we have a lot of work to do in the U.S. If the recovery is going to be consumer-led in the United States in 2010, it’s very early to be predicting consumer sentiment and confidence. We’ve gone from a nation that spent too much to one that arguably is saving a little too much right now, and until that behavior changes, I don’t see where the consumer-led recovery comes from.

I also don’t believe a lot of the stimulus money in the U.S. has been put to work yet. If I’m right about that, and it starts to show up in a meaningful way in 2010, that should help the situation. So the worst is definitely over, but there is a longer road to travel than a lot of people think.

For an emerging market like China, were you surprised at how quickly the government started its stimulus program and at the impact it has had?

In many ways, China is not really an emerging market anymore – they’ve emerged. Part of their speed was made possible by the government having a more centralized decision-making process, a structure that has some benefits in a time of crisis where you’re trying to move quickly. In other more decentralized decision-making countries, you have more debate over where the money is most optimally spent. The Chinese saw this crisis as a wake-up call. They had been too reliant on exports, so they took the opportunity to create infrastructure in the rest of the country outside of the urban areas, and they moved quickly because they anticipated that the growth rate was going to drop off. Even so, they still targeted 7.5 to 8 percent growth for 2009, which everybody thought was misguided at the time. But they achieved 8 percent in 2009, and it will be probably higher in 2010. So it was a big advantage for them to have that more centralized decision-making process. They also realized that if they moved quickly, they would come out of the crisis sooner than the rest of the world, and that accelerates their rebalancing of the global economy.

There are 79 listed companies on NYSE Euronext markets from Greater China. Do they represent a broad range in size and scale, and what is the growth potential in that market for you?

In addition to the 79 companies we have now, we anticipate many more new listings from China in 2010. Three or four years ago, the companies we had were mostly the state-owned enterprises (SOEs), because the first companies that came public in the United States capital markets from China were the SOEs. But there is a greater mix of business now, so we’re getting into health care, biotech, education, and clean energy. It’s not just SOEs – these are all shapes and sizes. Now that we have the NYSE platform and the NYSE-Amex platform – the latter for the small-and-medium-enterprise (SME) type of companies – a lot of our growth is going to come from the SMEs, who are on their way to becoming great companies. We’re not only relying on the SOEs coming here anymore, so I’m excited about the growth prospects.

Is the Indian market still offering great opportunity, and for the NYSE, how strong has that market been?

In terms of our relationships with listed companies, it continues to be quite good. I’m a big believer in India because it doesn’t have the reliance on exports that some of the other emerging countries do. India is quite satisfied with the growth it had in 2009, because it was created mainly by domestic demand. Other countries are struggling to create the domestic demand that India naturally has. So I’m very bullish in the near term on India, and you’re going to see more great companies coming out of India that want to access the U.S. and European capital markets.

Russia hasn’t had much growth over this past year, and many talk about it as a challenging place to do business. Has it been a key focus for the exchange?

With so few Russian companies listing in the U.S. in recent years, Russia has not been a top priority for us, but we are trying to make it a focus again. We can compete very effectively with what the London Stock Exchange (LSE) is offering on the NYSE Euronext side, so there’s a good chance that the next Russian company that accesses the capital markets outside of Russia is going to choose NYSE Euronext instead of the LSE. We have a better trading model – it’s not a separate board where we trade the international stocks. You trade on the same platform that all the other European companies are listed on and that NYSE Euronext trades on. The LSE has a separate international board, and a different liquidity profile and market structure. We don’t believe in that for NYSE Euronext. But the Russians didn’t know what NYSE Euronext was; we hadn’t effectively sold it to them. It’s a region we gave up on a few years ago and we are now reintroducing ourselves to them.

You have 31 listed companies in Brazil. How great is the opportunity in Brazil, and is all that the NYSE platform offers well understood in that market?

It is well understood in Brazil. There are 32 companies that have access to capital markets outside of Brazil, and 31 of them are listed with us, so our track record speaks for itself. We have broad and deep relationships throughout the country. There are plenty of companies that want to access the U.S. capital markets, and we have the advantage of being in the same time zone. In almost every case in which there is a company listed locally in Brazil as well as on the NYSE, it has added to the liquidity of that company’s underlying security. So the value proposition sells itself, because we have tangible evidence of what happens when you do list. Part of our success in this market is because as developed as the Brazilian equity market has become, it still has a ways to go. But when you have two pretty deep markets trading effectively in the same time zone, it increases the liquidity exponentially, and those Brazilian companies then become better known to all the U.S. investors that they’re hoping to attract as owners of their stock. There is an enormous pipeline for us there. We’re going to have a lot more Brazilian companies listed in the next two or three years.

Has the message about what the NYSE Amex platform offers reaching the SME-type companies that might benefit from it?

We’re doing a better job getting it out. The NYSE’s brand was never associated with having an SME platform, yet between the NYSE Amex in the U.S. and the NYSE Alternext in Europe, we have the biggest SME platform in the world. Now it’s our job to communicate that to people who would be interested in it.

We’re starting to find evidence that people are hearing the message; 2009 was a year in which a large number of Chinese companies came to list with us on the NYSE Amex platform. We never had an option for those companies before we did the Amex deal. With the Amex platform, they’re able to come into the family; we’re able to help them get more liquidity in their stock, and to get a higher profile and more visibility. As their success grows, they can move up to NYSE. So the message is starting to resonate, but we still have more work to do.

The NYSE brand has been transformed with the addition of Euronext and Amex. Is it challenging to get that message out within all the of different segments?

Our rich history is a blessing a majority of the time, but a lot of people don’t know how much we’ve transformed the business, and it’s our job to communicate it comprehensively. It’s a young public company – the NYSE/Euronext merger was two years ago and the Amex acquisition was a year ago – so in fairness to everybody here, we’re getting better at it, but we still have a long way to go, because small growth companies don’t know we have an interest in them. The fact is, we do; the proof of our value is in the results, and we’ve built a listings platform that now accommodates companies of all shapes and sizes around the world. We just need to do a better job of messaging that.

While everyone seems to be focused on China, are there strong opportunities for you in other emerging markets within Southeast Asia as well?

In all the Southeast Asian markets, like Vietnam, Philippines, Thailand, Malaysia, Taiwan Singapore, and a little in Hong Kong, there are great opportunities, but we’re going to have to be patient. Japan is pretty developed – we’ve got 15 or 20 great companies from Japan. I don’t believe there are another 15 or 20 that have a focus on being listed in the U.S. or European capital markets. Most of the great Japanese brands and great companies feel as though the investors already know who they are, and they already have some investors from around the world. So the opportunities in Asia are there, but our prospecting there right now is rather selective.

What about the prospects in Latin America?

Outside of Brazil, with a three- to five-year view, there will be great companies emerging from Chile, and we’ll see a few more from Argentina; Peru, and Columbia. But right now, Latin America is really the Brazil story. The Mexicans are also doing some interesting things where, if it becomes a bit more common to access the public markets, a lot of those companies could benefit greatly by also being listed in the markets here.

From a leadership point of view, how challenging has it been from the communications side, internally and also with your members, to get the message out about the exchange and the stability in the markets?

I don’t think it has been a challenge because we’ve been very focused on it, and one of the things we’ve done well during the past 12 months is to over-communicate internally, because we realize people want to hear more than just how the company is doing; they need to be reassured as to what is going on with regard to the external factors they don’t have control over. We always say to our team that we can only control what we can control, so let’s worry about that, and the rest will take care of itself. And that works, except in a crisis situation. In a crisis situation, people aren’t satisfied. They want some reassurance that we are taking steps to help be part of the solution to stabilize the situation. We shared that message externally as well, and we’ve taken more of a leadership role than we typically would, not as a lobbyist but as an advocate. We reminded the legislators how we performed during the crisis. We reminded them that an exchange is an important part of the financial infrastructure of any country, and if we need to be relied on to do more, we can be counted on. We’ve been pretty pragmatic in our approach, no matter whether it’s talking to the administration about tax policy or corporate governance. We’ve been equally pragmatic with the SEC in talking about potential changes to market structure that would re-instill investor confidence. So our employees are thirsty for it and we’ve been giving it to them. And the regulators and legislators are happy to hear from us right now because, in the broader financial services industry, we’re counted among the most independent, the most credible, and the least tainted. We didn’t contribute to the crisis. If anything, we helped stabilize things during and after the crisis, and that gives us a platform from which to speak that we don’t normally have, and it’s my responsibility to use that responsibly.